In partnership with

Welcome back, and a warm welcome to the 172 new subscribers who have joined FWDstart since our last deep dive! 👋

In our next two editions, we’ll be focusing on cloud kitchens. This week, we’ll dive into the current state of the cloud kitchen industry in MENA, examining its growth drivers, business models, major players, and what the future may hold.

Then, in two weeks, we’ll dedicate a case study exclusively to Kitopi, MENA’s fastest unicorn. We’ll go in-depth on the company’s origins, product, evolving business model, culture, and future outlook.

If you’re enjoying FWDstart, please consider sharing it with a friend. Your support makes a big difference, and we appreciate it enormously.

Free Notion and Unlimited AI

Thousands of startups use Notion as a connected workspace to create and share docs, take notes, manage projects, and organize knowledge—all in one place. We’re offering 3 months of new Plus plans + unlimited AI (worth up to $3,000)! To redeem the Notion for Startups offer:

Submit an application using our custom link and select Beehiiv on the partner list.

Include our partner key, STARTUP4110P67801.

The late, great chef and travel documentarian Anthony Bourdain once observed:

“To want to own a restaurant can be a strange and terrible affliction. What causes such a destructive urge in so many otherwise sensible people? Why would anyone who has worked hard, saved money, often been successful in other fields, want to pump their hard-earned cash down a hole that statistically, at least, will almost surely prove dry?”

Far be it for me to disagree. Restaurants face notoriously thin margins, high failure rates, and intense operational demands. This complexity and unpredictability has driven many would-be entrepreneurs to steer clear of the industry altogether.

Yet some persist — the operators, poets, and artisans who dedicate themselves to the craft, creating immersive experiences that nourish not just the body but the soul, leaving the world richer for their passion.

But, if we may be blunt: at its core, food is fuel — cells and nutrients, calories and sustenance. It’s this fundamental nature that the business of food ultimately serves, whether creatively or pragmatically.

Why, then, has art triumphed over science for so long in the restaurant world?

Paul Graham’s 2012 essay, Schlep blindness, may offer a window into this question. Graham describes “schlep blindness” as our tendency to avoid tedious, unglamorous problems, even when they’re valuable to solve. He writes:

“There are great startup ideas lying around unexploited right under our noses. One reason we don't see them is a phenomenon I call schlep blindness. Schlep was originally a Yiddish word but has passed into general use in the US. It means a tedious, unpleasant task.”

Few challenges fit the definition as perfectly as running a restaurant. It’s an unglamorous, operationally intense business that demands precision and perseverance.

And yet, perhaps it took someone from outside the restaurant world to see the value in solving these schleps. When Travis Kalanick of Uber infamy made his high-profile entry into the space with his purchase of CloudKitchens in 2018, people sat up and took notice.

But long before Kalanick’s foray, cloud kitchens had already been gaining traction in markets like India and Singapore.

And the GCC, it turned out, was perhaps the most fertile ground of all for cloud kitchens to take root.

The remainder of this article is for paid subscribers only.

Get access to the strategies, tactics, and wisdom of MENA's best investors, founders and operators with a paid subscription.

A mix of high basket sizes, a strong culture of food delivery, and relatively low labor and operational costs has created the perfect storm for favourable margins and unit economics.

At their core, cloud kitchens address a complex logistical challenge: optimising food production and delivery without the traditional restaurant front-of-house.

This requires intricate planning, technology integration, and seamless supply chain management — exactly the kind of schlep most people would rather avoid.

But for those willing to tackle it, cloud kitchens have unlocked new possibilities, meeting rising demand with a model that’s efficient, scalable, and resilient.

Below, we’ll explore the state of the cloud kitchen industry in MENA today, its growth drivers, business models, major players, and what the future may hold.

Let’s dig in.

The remainder of this newsletter is for paid subscribers only.

Don’t miss out! Become a member today.

A subscription gets you full access to our weekly deep-dives, which include:

✅ Analysis, case studies and interviews unpacking trends, companies, or industries, and more.

✅ Access to the strategies, tactics, and wisdom of MENA's best investors and founders.

✅ Practical and actionable guides designed to make you a better investor and technologist.

✅ Unlimited access to our online archive where you can read previous editions of the newsletter.

🍴 Rethinking restaurants

Kitopi’s CEO, Mohamad Ballout

Food delivery aggregators like Talabat and Deliveroo built a model around food prepared for delivery — a product that traditional restaurants were never designed to provide.

These restaurants were accustomed to plating meals for dine-in guests, not packaging them for a 20-minute motorbike ride. Preparing food for rapid assembly and delivery posed unique challenges.

A typical restaurant might handle 15-20 delivery orders per hour, while a cloud kitchen can process up to 60 with just one employee.

Cloud kitchens are engineered to remove delivery bottlenecks: the layout resembles an assembly line, where everything is prepped in sequence, maximising speed and minimising movement.

In essence, cloud kitchens are designed to maximise utilisation and revenue per square foot.

This efficiency has led to a couple of dominant models:

Kitchen-as-a-Service (KaaS)

Virtual Brands

Rent a Kitchen Space

Fully Stacked Integrated Kitchen Model

🥭 Ripe conditions

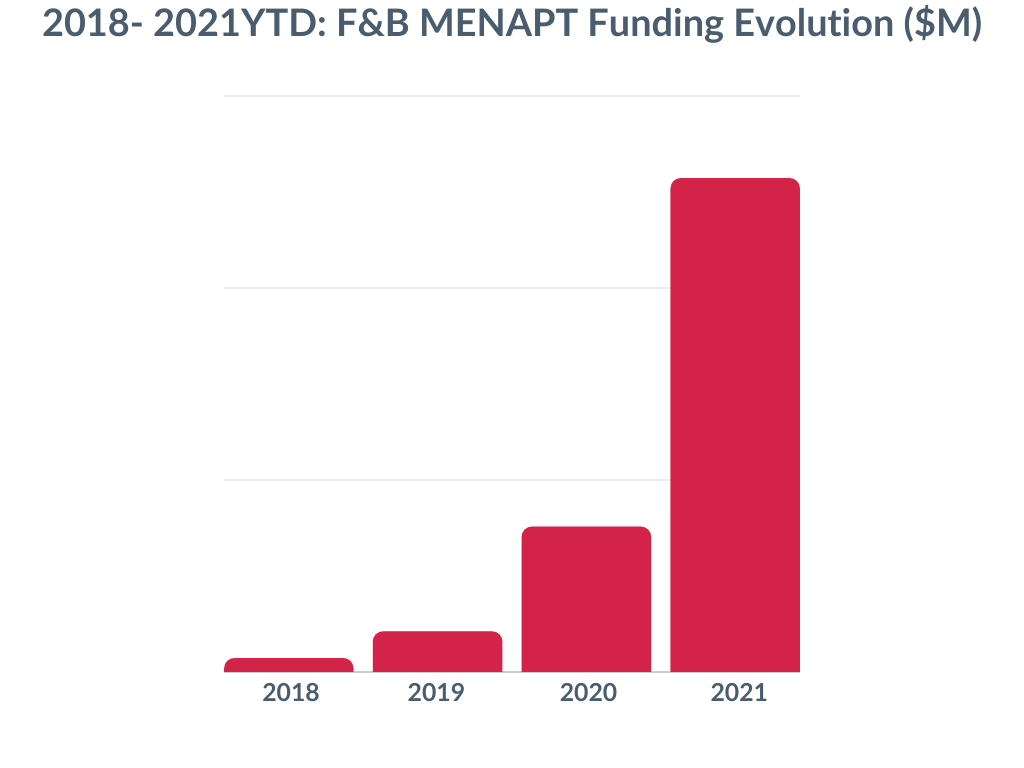

The GCC quickly became a global hotspot for cloud kitchens, with revenues in the UAE and Saudi Arabia surging 160% from 2018 to 2019 to exceed $65 million.

A confluence of factors contributed to this growth:

High consumer acceptance: The Middle East and North Africa (MENA) region is one of the most lucrative for online food delivery, valued at $3 billion in 2021. The UAE and Saudi Arabia alone account for close to $2 billion of this.

Strong ARPU (average revenue per user): Kuwait, for example, boasts an ARPU of $498 — among the highest in the world. For comparison, the U.S. ARPU is $235, the UAE’s is $356, and Saudi Arabia’s is $194.

Pandemic tailwinds and capital flow: COVID-19 accelerated demand for delivery, drawing investor interest. In 2021 alone, UAE-based cloud kitchen startups attracted significant investment. Kitopi led the charge with a $415 million Series C, followed by iKcon ($20 million Series A), Kitch ($15 million Series A).

Together, these factors made the GCC a fertile environment for cloud kitchens.

Source: MAGNiTT

Within the cloud kitchen space, various business models have emerged. However, with consolidation among the largest players, the range of models has narrowed over time.

💰 Reinventing the wheel to go back again

Cloud kitchens have arguably evolved through three primary waves:

First came satellite kitchens, which dominated the market by leasing space to existing restaurants for delivery operations.

The second wave introduced Kitchen-as-a-Service (KaaS) and virtual restaurants and brands, often operating within those same satellite kitchens.

The third wave brought consolidation and the emergence of the fully stacked integrated restaurant model as the preferred for market leaders.

🌱 Phase 1 and 2

The initial B2B Kitchen-as-a-Service (KaaS) model provided kitchen space and operational support to established restaurants and emerging virtual brands alike.

Startups like Kitchen Nation and OneKitchen (both now defunct, a sign of the direction of travel) offered fully equipped kitchens to brands or individual operators on a monthly fee basis, functioning like co-working spaces for chefs.

Operators such as iKcon and Kitopi took this model a step further. They didn’t just lease kitchen space; they staffed kitchens with chefs who prepared meals for partner brands, which were then listed on food delivery platforms.

IKcon founders Khalid Baareh and Kareem Abughazaleh

This KaaS model allowed brands to scale distribution across a city without the high costs of setting up new locations. By listing on third-party aggregator platforms, these brands gained immediate access to a broad customer base.

For example, Kitopi retained around 85% of the revenue from each brand it partnered with, paying back 10-13% in royalties along with a dedicated marketing budget. iKcon operated with a similar structure.

One notable partnership was between Kitopi and The Leap Nation, which offered 13 brands ranging from fried chicken to freekeh bowls. By outsourcing everything but menu design and brand identity, Leap Nation could swiftly adjust to consumer demand. If a dish underperformed, it could be quickly removed from the menu, minimising financial risk.

Meanwhile, other operators like The Cloud implemented a different strategy within the KaaS model, maximising existing kitchen space by launching virtual brands within established restaurant kitchens.

This approach leverages a restaurant’s unused capacity to expand revenue without adding locations — a method Olaf Abi Aad, founder of The Cloud, likens to a diffusion line in fashion, catering to diverse market segments efficiently.

An example of a diffusion line in fashion, using Giorgio Armani

🌳 Phase 3

Kitopi initially operated as a B2B provider, helping restaurants expand via a centralised kitchen model.

But just before its SoftBank-led Series C, Kitopi pivoted to a B2C strategy, shifting from licensing brands to acquiring them outright.

Talk about interesting timing.

The rationale? While the B2B model allowed rapid, cost-effective expansion, it left Kitopi invisible to consumers who remained unaware their food came from a Kitopi-operated kitchen.

Additionally, delivery aggregators, controlling customer relationships and data, began to squeeze Kitopi’s position. This likely led founder Mohamad Ballout to question Kitopi’s sustainability as a B2B player amid aggregator dominance.

It’s similar to the concerns Mark Zuckerberg had about Facebook’s dependence on Apple’s App Store, where control over user access and relationships rested with a third party.

The solution was to expand into B2C, build brand recognition, and own the customer relationship directly. As Ballout noted, “The real problem wasn’t for restaurants but for the customers,” seeing a consumer-first approach as far more lucrative than staying B2B.

This pivot involved substantial changes, moving from tech licensing to full brand acquisition.

Now, if you order from one of 300 brands in the region, Kitopi manages the entire process — from preparation to delivery. While still partnering with platforms like Deliveroo and Talabat, Kitopi’s pivot has allowed it to retain brand ownership and visibility with consumers.

Other fully integrated players in the region, such as Krush Brands and Epik Foods, are expanding similarly.

Only this week, Abu Dhabi-based Ruya Partners invested $15.5 million in Epik Foods to support its growth in Saudi Arabia and the UAE.

Formed through the merger of three UAE food-tech players, Epik Foods now oversees a portfolio of 60 brands across 50 locations, with 20 more in the pipeline. This investment aims to fuel further acquisitions, setting the stage for continued consolidation in the space.

🤏 Consolidation

The foodtech space has been a relative hive of M&A activity over the past number of year as capital-flush operators focus on securing their positions in an expanding market.

Kitopi’s monumental Series C, which eventually totalled $715 million, catalysed much of this activity.

Shifting its strategy from licensing to outright ownership, Kitopi has acquired multiple regional virtual restaurant groups, including Cloud Restaurants, Leap Nation, Right Bite, Under500, Ichiban, and most recently, AWJ Group.

This consolidation trend is also evident with companies like Sweetheart Kitchen and iKcon.

Sweetheart Kitchen, acquired by Delivery Hero, streamlined its operations to efficiently manage multiple brands, raising $42.5 million and achieving significant economies of scale.

Similarly, iKcon was acquired by REEF Technology, North America’s largest cloud kitchen operator, marking REEF’s entry into the MENA region. This acquisition extends REEF’s network to over 5,000 cloud kitchen hubs, backed by $1.5 billion from investors, including Mubadala and SoftBank.

🍽️ What’s next?

At a fireside chat at FII7 in Riyadh, Kitopi’s CEO Mohamad Ballout hinted that the company could be gearing up for an IPO within the next 18 months.

That timeline is now quickly approaching. Kitopi reported $330 million in revenue last year and achieved EBITDA positivity.

In our next deep dive, we’ll place Kitopi under the microscope to explore exactly how it became MENA’s fastest unicorn and what the future might hold.

Stay tuned.

👋 Message from the team

Thanks for reading this week’s edition!

If you’re enjoying the newsletter, don’t forget to share it with a friend!

Have a question or any feedback? Just hit reply, or provide a rating below - we want to hear from you!!

How was this newsletter edition?

Was this forwarded to you? Sign up here.